How to Get Prequalified for a Car Loan: A Step-by-Step Guide

May 19, 2026

If you’re planning to buy a car, getting prequalified for a car loan before you visit a dealership is one of the smartest financial moves you can make.

Pre-qualification tells you what you can realistically afford, and what your estimated monthly payment will be. It also gives you confidence and negotiating leverage when you sit down at the dealership.

This guide walks you through getting prequalified for a car loan step by step, what lenders look for, what you need ready, and how to make the most of the process.

What does getting prequalified for a car loan mean?

Getting prequalified for a car loan means a lender has evaluated your financial profile and provided you with an estimated loan amount, interest rate, and term.

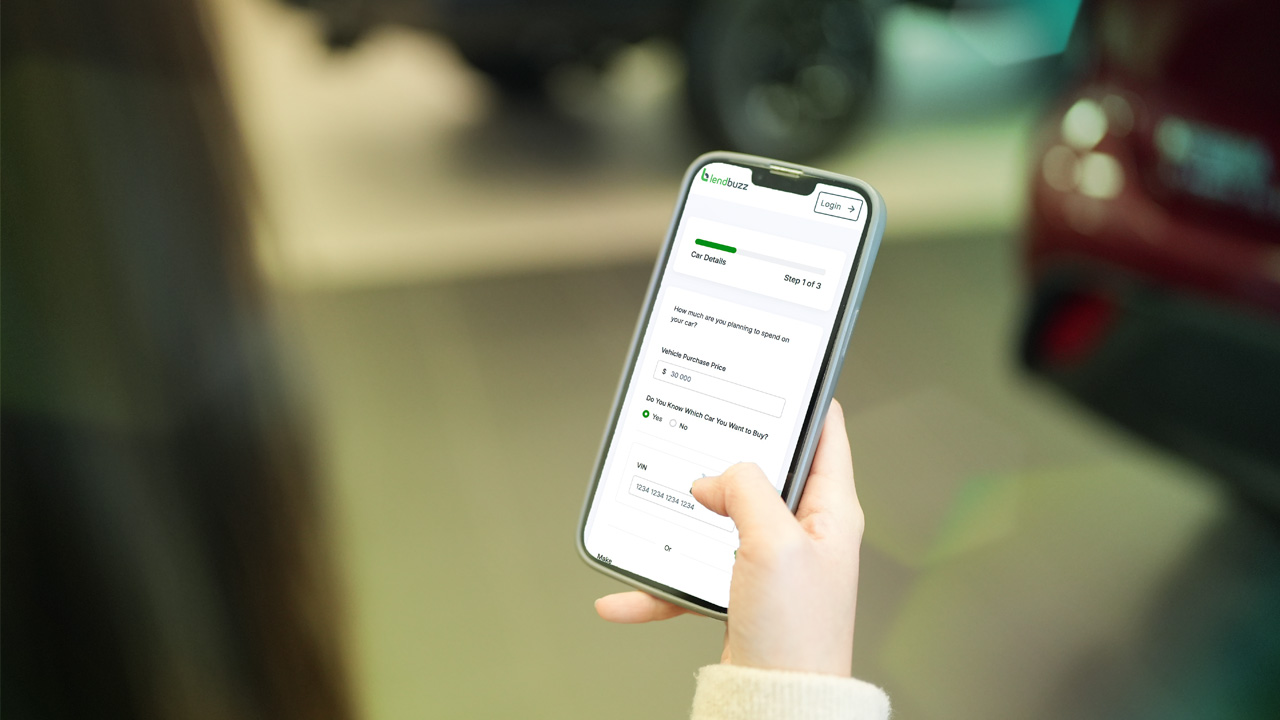

At Lendbuzz, pre-qualification is the first step in the financing process. You share your basic information, and our AI-powered platform assesses your creditworthiness to give you a personalized rate and terms you can use to shop.

How does auto loan prequalification work in practice? You submit a short application (online or on your phone), the lender evaluates your profile, and if you qualify, you receive a rate, loan amount, and estimated monthly payment.

You then shop for a vehicle within that budget.

When you find the right car, you take your pre-qualification to a participating dealership, and the dealer finalizes the deal.

How is pre-qualification different from pre-approval?

At Lendbuzz, pre-qualification and pre-approval are two distinct steps in the financing process.

Pre-qualification is the borrower-side evaluation. You submit your information, and Lendbuzz assesses your financial profile to provide an estimated rate and terms. This gives you a clear picture of what you can afford before you start shopping.

Pre-approval goes a step further. When you connect your bank account through Plaid and complete the full verification process, Lendbuzz's AIRA technology conducts a deeper analysis of your income, financial behavior, and banking history.

The result is a firmer, verified offer based on a more complete picture of your finances.

Final approval happens when the full deal comes together: your borrower profile, the specific vehicle, and the deal structure are all confirmed. Pre-qualification starts that process by telling you where you stand before you ever set foot in a dealership.

The takeaway: pre-qualification is the fastest way to establish your budget and rate. The further you go in the process (connecting your bank, selecting a vehicle, finalizing the deal), the more concrete your terms become.

How to get prequalified for a car loan: Step-by-step guide

How do you get prequalified for a car loan? The process is straightforward, but a little preparation makes the difference between a good deal and a great one.

Step 1: Check your credit score and report

Before you apply anywhere, pull your credit report from all three bureaus at AnnualCreditReport.com.

Check for errors, incorrect balances, or accounts that aren’t yours. Disputing and correcting mistakes can raise your score enough to qualify for a better rate tier.

Knowing your score also sets realistic expectations for the terms you’ll receive.

That said, some lenders (like Lendbuzz) evaluate far more than your credit score, so don’t let a lower number discourage you from applying.

Step 2: Decide how much car you can afford

Before you apply for pre-qualification, set a budget.

A common guideline is to keep your total car payment (loan, insurance, fuel, maintenance) below 15% to 20% of your monthly take-home pay.

Factor in your down payment and any trade-in value.

Having a target number prevents you from overextending, and pre-qualification will confirm whether your target is realistic.

Step 3: Gather your information

Most lenders will need your basic personal information, income details, and identification.

Traditional lenders typically ask for paper pay stubs, W-2s, or tax returns, plus proof of residence and a government-issued ID.

Lenders using AI-powered underwriting (like Lendbuzz) can verify income and financial health digitally through your bank account via Plaid, which eliminates most paper document requirements.

At minimum, have your Social Security number or ITIN, a rough idea of your income, and a government-issued ID ready.

Step 4: Compare lenders and apply

This is the most important step when asking, “How do I get prequalified for a car loan at the best rate?” The answer is by comparing offers from at least three sources: your bank or credit union, an online lender, and a lender that uses AI or alternative data.

Many lenders let you pre-qualify with a soft pull first, so you can compare rates without affecting your credit score.

If you apply to multiple lenders within a 14-day window, the credit bureaus typically group hard inquiries as a single event.

Prioritize lenders that offer soft pull pre-qualification so you can shop freely.

Step 5: Review your pre-qualification offer

When your pre-qualification comes back, review the loan amount, interest rate, loan term, and estimated monthly payment.

Understand what’s firm and what may adjust when you finalize the deal.

At Lendbuzz, your pre-qualification gives you a personalized rate based on your financial profile. That rate may adjust slightly when the full deal (including the specific vehicle and deal structure) is submitted, but in most cases, the difference is minimal.

Step 6: Shop for your vehicle and close the deal

Take your pre-qualification to a participating dealership. Focus on negotiating the price of the vehicle separately from the financing. If the dealer offers their own financing, compare it against your pre-qualified rate.

Accept whichever gives you the better total cost.

Once the deal is finalized and submitted, the lender completes the approval process and funds the loan.

Benefits of getting prequalified for a car loan

You know your real budget before shopping

Pre-qualification removes the guesswork. Instead of browsing inventory, wondering what you can afford, you know your estimated loan amount and monthly payment.

This saves time and prevents emotional decisions at the dealership.

Stronger negotiating position at the dealership

When you have a pre-qualified rate in hand, the dealer cannot pressure you into a higher-rate loan without you knowing the difference. You can compare their financing offer against your pre-qualification and choose the better deal.

This leverage alone can save you hundreds or thousands of dollars over the life of the loan.

Faster, smoother closing

The financing conversation at the dealership takes minutes, not hours, when you already have a pre-qualified offer. This is better for you (less time waiting) and better for the dealer (faster turnaround).

Should you get prequalified for a car loan before going to the dealership? For this reason alone, yes.

Easier to compare offers side by side

Getting prequalified for a car loan with multiple lenders lets you line up rates, terms, and fees in a direct comparison.

Without pre-qualification, you’re relying on the dealer to find you the best rate, and their incentives aren’t always aligned with yours.

Potential drawbacks of getting prequalified for a car loan

Some lenders use a hard pull for pre-qualification

Some lenders require a hard credit pull even for pre-qualification, which can temporarily lower your score by a few points.

However, multiple auto loan inquiries within a 14-day window are grouped as one.

Plus, lenders that offer soft pull pre-qualification (like Lendbuzz) let you check your rate with zero credit impact.

Pre-qualification offers expire

Most pre-qualification offers are valid for 30 to 60 days, with some lenders offering up to 90 days. If your offer expires before you find a car, you’ll need to reapply.

To make the most of your window, start shopping soon after you receive your pre-qualification and have a general idea of what type of vehicle you want before you apply.

The final rate is not guaranteed until the deal closes

A pre-qualification gives you an estimated rate based on your borrower profile.

The final rate may adjust when the full deal is submitted, including the specific vehicle, deal structure, and current market conditions.

In most cases, the adjustment is minor, but it’s important to understand that pre-qualification is an estimated offer, not a signed contract.

What do you need to get prequalified for a car loan?

Credit and income considerations

Requirements vary by lender.

Traditional banks typically want a credit score of 660 or higher and verifiable income. Credit unions may be more flexible for members.

AI-powered lenders like Lendbuzz evaluate bank account data and financial behavior rather than relying solely on FICO scores, allowing them to pre-qualify borrowers with thin files, no credit history, or non-traditional income sources.

There’s no universal minimum credit score for pre-qualification across the industry.

What to have ready

At minimum, have your government-issued photo ID, your Social Security number or ITIN, and a general sense of your income and employment.

Traditional lenders may also ask for paper pay stubs, W-2s, proof of residence, and bank statements.

Lenders that verify income digitally through Plaid may not require any paper documents at all, making the process significantly faster.

How long is a car loan pre-qualification good for?

Most auto loan pre-qualifications are valid for 30 to 60 days, though some lenders extend the window to 90 days.

During that period, you can shop at dealerships using your pre-qualified terms. If the offer expires, you can usually reapply, but a new inquiry may be required depending on the lender.

Start shopping shortly after receiving your pre-qualification and have a general idea of what vehicle you want before you apply.

Questions to ask before getting prequalified for a car loan

What is the interest rate and APR?

The interest rate is what the lender charges to borrow. The APR includes the rate plus any fees, giving you the true annual cost of the loan.

Always compare APR, not just rates, across lenders.

Is the pre-qualification based on a soft pull or hard pull?

A soft pull doesn’t affect your credit score. A hard pull does (slightly and temporarily).

If you want to compare multiple lenders before committing, prioritize those offering soft pull pre-qualification first.

Are there origination fees or prepayment penalties?

Some lenders charge origination fees that get added to your loan balance. Others penalize you for paying off the loan early.

Ask about both before applying. The best lenders charge neither.

Is the pre-qualification tied to a specific vehicle?

Most pre-qualifications are borrower-based, meaning you can use them for any qualifying vehicle within the estimated loan amount.

Some lenders may restrict by vehicle age, mileage, or type. Clarify this before you shop.

Red flags to watch out for when getting prequalified for an auto loan

Interest rates well above market with no explanation

If a lender offers a rate that’s significantly higher than what you see from other sources for your credit tier, ask why.

If they cannot give a clear answer, move on. Predatory lenders count on borrowers not shopping around.

Pressure to decide immediately

A legitimate pre-qualification doesn’t require a same-day decision.

If a lender or dealer pressures you to commit before you have had time to compare options, that’s a warning sign.

Take the offer home, review the terms, and compare.

Hidden fees buried in the paperwork

Read every document. Look for origination fees, processing fees, dealer markup on the rate, and prepayment penalties.

If you cannot get a clear breakdown of all costs in writing, don’t sign.

Lenders who do not check your ability to repay

A lender that pre-qualifies you without verifying income or financial health isn’t doing you a favor. They may be setting you up with a loan you cannot afford, which leads to default and repossession.

Responsible lenders verify your ability to repay. That’s a feature, not a burden.

Should you get prequalified for a car loan?

Should I get prequalified for a car loan? For the vast majority of car buyers, yes.

Pre-qualification is the right move if you’re planning to visit a dealership, financing a significant amount, want negotiating leverage, or want to confirm your rate and budget before committing to a vehicle.

Pre-qualification may matter less if you’re paying cash, already qualify for a manufacturer's promotional 0% APR (these are typically offered only to super-prime borrowers with 780+ scores), or buying from a private seller with funds already in hand.

For everyone else, the few minutes it takes to get prequalified can save you thousands of dollars and hours of frustration.

Is it better to get prequalified for a car loan before going to the dealership? Almost always.

Ready to get prequalified?

Lendbuzz makes getting prequalified for a car loan fast, simple, and risk-free. Our AI-powered platform looks beyond your credit score to offer personalized rates based on your real financial picture.

The application takes 2 minutes on your phone, uses a soft pull with no credit impact, and most borrowers receive their decision the same day.

Whether you’re a first-time buyer, rebuilding credit, or financing with an ITIN, Lendbuzz can help.

How to get prequalified for an auto loan: Key takeaways

Getting prequalified before visiting a dealership gives you a clear budget, an estimated rate, and real negotiating leverage.

The process involves checking your credit, setting a budget, gathering your information, comparing lenders, and applying with the best option.

Pre-qualification is the first step in Lendbuzz's financing process, followed by pre-approval (after full bank verification) and final deal approval.

Always compare at least three lenders, prioritize those that offer soft-pull pre-qualification, and read every document before signing.

Pre-qualification offers typically expire in 30 to 60 days, so start shopping soon after you receive yours.

FAQs

How does auto loan prequalification work?

You submit your financial information to a lender, and they evaluate your profile to provide an estimated rate, loan amount, and term.

At Lendbuzz, this means our AI analyzes your financial data and returns a personalized offer.

You then take that pre-qualification to a dealership, choose a vehicle, and the lender finalizes the deal.

Does getting prequalified for a car loan hurt your credit?

It depends on the lender.

Some use a hard pull, which can cause a small, temporary score decrease. Others (like Lendbuzz) use a soft pull for pre-qualification, which has zero impact on your credit score.

Always ask whether the process involves a soft or hard inquiry before applying.

Can you get prequalified for a car loan online?

Yes. Many banks, credit unions, and online lenders offer fully digital pre-qualification.

The entire process, from application to rate confirmation, can happen on your phone or computer in minutes.

Online lenders that use AI and digital bank verification tend to be the fastest.

Can you get prequalified for a car loan with bad credit?

Yes, though your options and rates will vary.

Traditional lenders may decline you or offer higher rates.

AI-powered lenders like Lendbuzz evaluate your full financial picture and can pre-qualify borrowers that FICO-only models miss.

A larger down payment and a cosigner can also improve your odds and terms.

What is the difference between pre-qualification and pre-approval for a car loan?

At Lendbuzz, pre-qualification is the initial step where you submit your information and receive an estimated rate and terms.

Pre-approval is the next step, where you connect your bank through Plaid and complete full income and financial verification, resulting in a firmer, more detailed offer.

Final approval happens when the complete deal (borrower, vehicle, and deal structure) is confirmed.

Each step adds more certainty to your terms.

Is it better to get prequalified for a car loan before going to the dealership?

Yes. Walking into a dealership with pre-qualification gives you a clear budget, a baseline rate to compare against dealer offers, and significantly more negotiating leverage.

Without it, you’re relying entirely on whatever financing the dealer presents, which may not be the best available to you.

How long does it take to get prequalified for a car loan?

It depends on the lender. Traditional banks may take one to three business days. Online lenders and AI-powered platforms can deliver a decision in minutes.

Lendbuzz, for example, completes most pre-qualifications the same day the application is submitted.

Can you get prequalified for a car loan at multiple lenders?

Yes, and you should. Comparing offers from multiple lenders is the most effective way to get the best rate.

If you apply to multiple auto lenders within a 14-day window, the credit bureaus typically group hard inquiries as a single event.

Lenders offering soft pull pre-qualification let you compare without any credit impact at all.

Can you get prequalified for a used car loan?

Yes. Most lenders offer pre-qualification for both new and used vehicles.

Some may have restrictions on vehicle age or mileage (for example, requiring the car to be less than 10 years old with under 100,000 miles).

Check with each lender for their specific used vehicle requirements.

Can you get prequalified for a car loan without affecting your credit?

Yes, if you use a lender that offers soft pull pre-qualification.

Lendbuzz checks your rate with a soft inquiry that has zero impact on your credit score.

A hard pull only occurs if you choose to finalize the loan. This lets you shop rates freely without risk.

Where is the best place to get prequalified for a car loan?

The best place is wherever you get the lowest rate for your specific financial profile.

Compare at least three sources: a bank or credit union, an online lender, and an AI-powered platform like Lendbuzz that evaluates alternative data.

Each type of lender serves different borrower profiles differently, so casting a wide net gives you the best shot at the best terms.

With over a decade in the retail automotive space, Ariana regularly writes on a variety of car dealer and car buyer/borrower-related subjects.