Bank Vs Credit Union Auto Loan: What’s Smarter in 2026?

February 20, 2026

When you need to finance a car, two options dominate the conversation: banks and credit unions. Both offer auto loans, but they operate differently and serve borrowers in distinct ways.

Understanding the bank vs credit union auto loan debate helps you choose the financing option that saves you the most money and fits your situation.

The short answer? Credit unions typically offer lower rates, but banks provide more convenience and product variety. The right choice depends on your credit profile, how much you're borrowing, and whether you're already a member of a credit union.

But there's also a third option worth considering: AI-powered lenders like Lendbuzz that combine competitive rates with modern convenience, especially for borrowers who don't fit neatly into traditional lending categories.

This guide breaks down everything you need to know.

Should You Choose a Credit Union or Bank for an Auto Loan?

Neither option is universally better. Credit unions are member-owned nonprofits that typically return profits to members through lower rates and fees. Banks are for-profit institutions with broader product offerings and more branch locations.

The question isn't which is better overall, but which is better for your specific needs.

If you already belong to a credit union and have good credit, starting there makes sense. If you don't have credit union membership or need a faster, more digital experience, banks and online lenders may serve you better.

And if you have thin credit or a non-traditional financial profile, specialized lenders like Lendbuzz often outperform both. Lendbuzz uses AI-powered underwriting and alternative data to evaluate borrowers beyond traditional credit scores, offering competitive rates to buyers that banks and credit unions may overlook.

Credit Union vs Bank Auto Loans: What Are the Differences?

Understanding how these institutions differ helps you evaluate their auto loan products more effectively.

Here are some of the main differences between the two:

1. Interest Rates

Credit unions consistently offer lower average interest rates than banks. Industry data show that credit union auto loan rates are approximately 1% to 2% lower than bank rates on average. Over a five-year loan, that difference can save you hundreds or even thousands of dollars.

Are credit unions better for auto loans purely on rate? Usually, yes, but rates vary by institution and your credit profile.

2. Membership Requirements

Banks accept anyone who meets their lending criteria. Credit unions require membership, which typically means meeting certain eligibility criteria: living in a specific geographic area, working for a particular employer, or belonging to an affiliated organization.

Some credit unions have open membership through associations that anyone can join, but you must become a member before applying for a loan.

3. Approval Process and Speed

Banks, especially large national institutions, often have more streamlined digital applications and faster approval processes. Many banks offer same-day or next-day decisions. Credit unions can be slower, particularly smaller ones with less automated underwriting.

If speed matters to you, it's worth noting that AI-powered lenders like Lendbuzz can match or beat bank approval times while still offering rates that compete with credit unions.

Our tech-driven underwriting process delivers fast decisions without sacrificing rate competitiveness.

4. Customer Service Approach

Credit unions are known for personalized service. As member-owned institutions, they have an incentive to treat you well. Banks vary widely. Large national banks may feel impersonal, while regional or community banks can offer a more relationship-focused experience.

Your experience depends on the specific institution.

5. Loan Terms and Flexibility

Banks typically offer more variety in loan terms, from 24 to 84 months or longer. They may also have more flexible policies on vehicle age and mileage. Some credit unions restrict loans to newer vehicles or cap the loan term on older cars.

Check specific policies before applying.

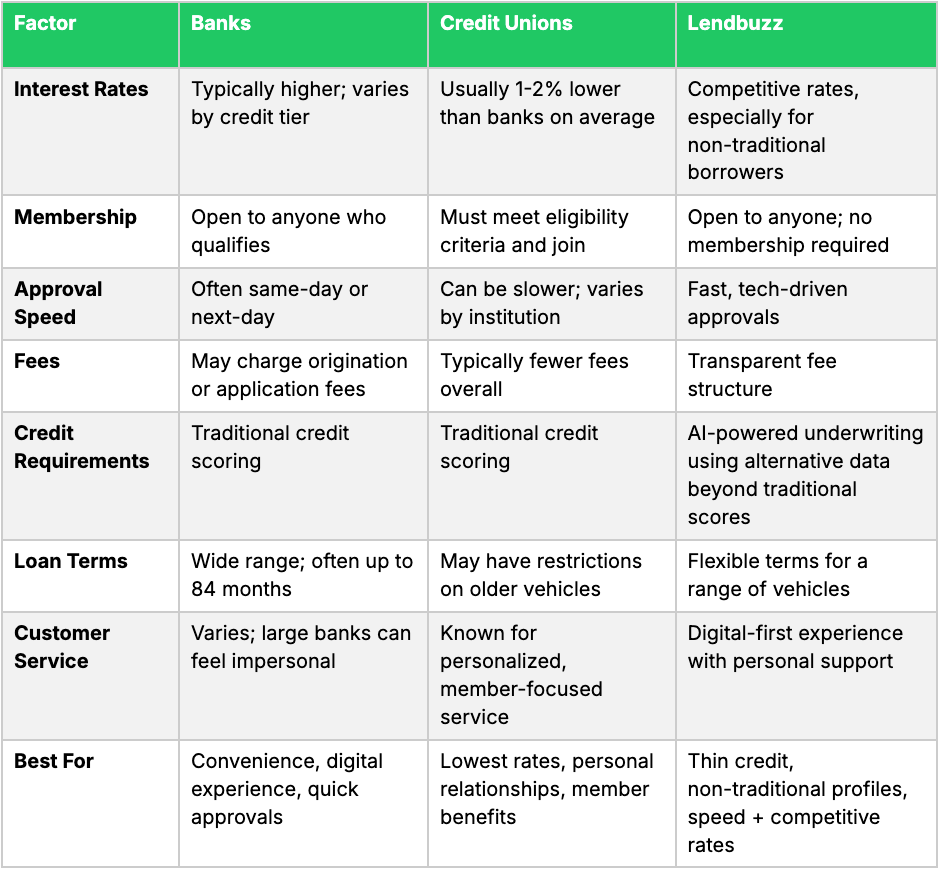

Credit Union vs Bank vs Alternative Lender: Side-by-Side Comparison

This comparison table summarizes the key differences between your main auto loan options:

Factors to Consider When Choosing Your Auto Loan

Beyond the general differences, several personal factors should guide your decision.

Here are some important factors to consider:

1. Your Current Credit Score and Financial History

If you have excellent credit (720+), you'll get competitive rates almost anywhere. The credit union advantage is most pronounced for borrowers in the good-to-fair range, where their lower average rates make a bigger difference.

If you have thin credit or a limited history, neither banks nor credit unions may be your best option.

Lenders like Lendbuzz specialize in exactly this scenario, using AI-powered risk analysis and alternative data sources to evaluate your full financial picture rather than relying solely on a traditional credit score. This approach opens doors for first-time buyers, recent graduates, and newcomers who haven't yet built a conventional credit history.

2. Total Amount You Need to Borrow

For larger loans, even small rate differences matter more. A 1% rate reduction on a $40,000 loan saves more than the same reduction on a $15,000 loan. If you're financing a significant amount, do the math carefully.

Use a car loan comparison calculator to see exactly how rate differences affect your total cost.

3. Preferred Loan Term Length

If you want flexibility on term length, banks often provide more options. Some credit unions cap terms on used vehicles or won't finance cars older than a certain year. Check specific policies before applying, especially if you're buying an older used car.

Understanding the difference between principal payment vs regular payment car loan can also help you choose the right term for your situation.

4. Existing Banking Relationships

If you already have accounts at a bank or credit union, they may offer relationship discounts on auto loans. Some institutions reduce rates by 0.25% to 0.50% for existing customers with direct deposit or other accounts. This can narrow or eliminate the typical credit union rate advantage.

5. Age and Type of Vehicle

Financing a new car is straightforward at either institution. Used cars get more complicated. Some credit unions won't finance vehicles over a certain age or mileage, or they charge higher rates for older cars. Banks and online lenders may have more flexible policies.

If you're considering financing a car through a dealership, compare those rates against bank, credit union, and alternative lender offers.

Key Takeaways

The credit union vs bank auto loan decision comes down to your priorities. Credit unions typically offer better rates and more personalized service, but require membership and may have slower processes. Banks provide convenience, speed, and flexibility, but often at higher rates.

Do credit unions offer better auto loan rates? On average, yes. Are credit unions better for car loans in every situation? Not necessarily. Your specific circumstances matter more than general averages.

The smartest approach is to get quotes from multiple sources: your bank if you have one, a credit union if you're eligible, and alternative lenders for comparison. The best rate is the one you actually qualify for, not the one advertised on a website.

For buyers with thin credit files, non-traditional income sources, or limited U.S. credit history, Lendbuzz offers a compelling third path.

Whether you're a first-time buyer, a recent immigrant, or simply someone who wants a tech-forward financing experience, comparing your options across all three lending categories gives you the best chance of finding the right rate and terms for your situation.

With over a decade in the retail automotive space, Ariana regularly writes on a variety of car dealer and car buyer/borrower-related subjects.